Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

What’s a Good Mortgage Rate in Nova Scotia March 2026? Fixed vs. Variable And How the Stress Test Affects Your Budget

By Rob Lough, Broker/Owner | Century 21 Optimum Realty | Halifax-Dartmouth, Nova Scotia Published: March 2026

If you’re buying a home in Halifax-Dartmouth or anywhere across Nova Scotia this spring, one of the first questions you’ll ask is: “What should I actually be paying for a mortgage?” It’s a fair question and the answer in 2026 is more nuanced than a single number. This article breaks down current rate territory, the fixed vs. variable debate, and how the federal stress test is quietly shaping what buyers can afford.

What’s a “Good” Mortgage Rate in Nova Scotia Right Now?

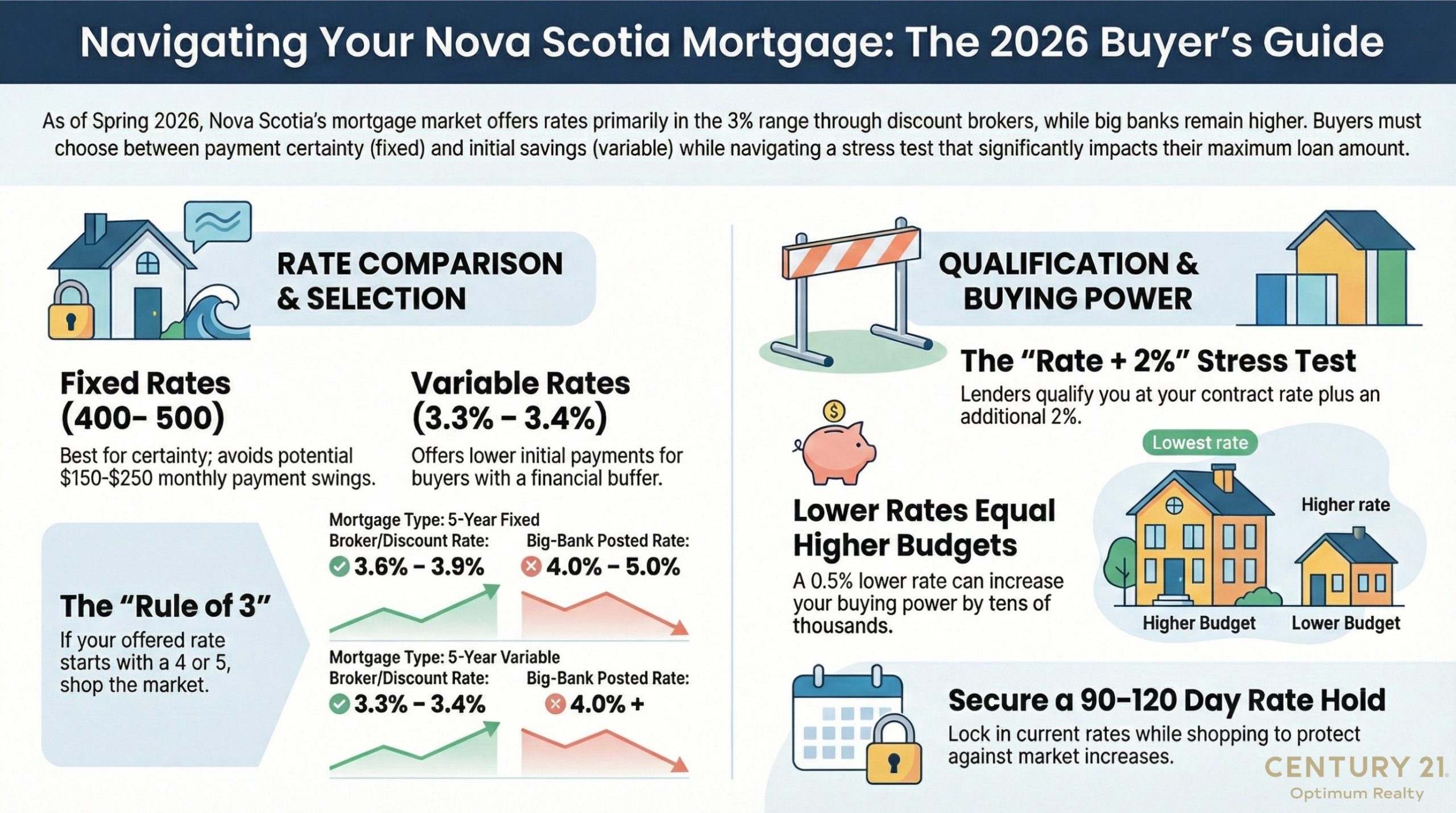

Let’s start with a baseline. As of late March 2026, competitive rates from deep-discount brokers and non-bank lenders in Nova Scotia are landing in roughly these ranges for well-qualified buyers:

- 5-year fixed: approximately 3.6–3.9% (deep-discount / broker channel)

- 5-year variable: approximately 3.3–3.4% (most aggressive offers, tied to prime)

Big-bank posted or walk-in rates are often still sitting in the 4–5% range for fixed terms. That gap matters, it’s not unusual for a buyer who “just takes the bank’s rate” to be paying 0.5 to 1.0% more than necessary, which translates to hundreds of dollars a month on a typical Halifax-area purchase.

A simple rule of thumb: if you’re seeing a rate with a “3” in front of it from a reputable, regulated lender, you’re in today’s competitive territory. If your bank’s first offer starts with a “4” or “5,” that number is almost certainly improvable. Shop the market, not the poster.

Use the mortgage calculator on this site to run your own numbers at different rate scenarios and the monthly payment difference between 3.7% and 4.5% on a $450,000 mortgage is significant.

Fixed vs. Variable in 2026: Who Should Choose What?

The fixed-versus-variable question is genuinely more nuanced right now than it has been in years. Here’s the plain-language version.

The Bank of Canada’s overnight rate, which drives variable mortgage rates, is expected to stay relatively stable through much of 2026, with only gradual upward pressure if inflation re-accelerates later in the year. That’s kept variable rates attractively priced for now. Meanwhile, bond yields (which drive fixed rates) have crept higher on geopolitical and inflation concerns, nudging fixed rates up roughly 0.30% recently with room for further movement.

The result is a genuine fork in the road for buyers.

Fixed Rate – Who It’s Best For

- Buyers who are close to their maximum qualifying budget and need payment certainty

- Those who would genuinely lose sleep over a $150–$250/month swing in their mortgage payment

- Anyone who values predictability over potential savings

A fixed rate means your payment and interest cost are locked for the term with no surprises even if the Bank of Canada moves.

The main trade-off: if rates stay flat or fall, you may pay slightly more in total interest than a variable borrower would have.

Variable Rate – Who It’s Best For

- Buyers with some financial buffer above their qualifying budget

- Those comfortable with the possibility that their payment or amortization could change

- Buyers who believe the Bank of Canada will stay on hold longer than markets currently expect

Variable rates are starting lower right now, which means lower initial payments and potentially less total interest paid if rates stay stable.

The main trade-off: payments or amortization can change if the Bank of Canada raises rates.

The practical 2026 rule of thumb: if a $150–$250/month payment increase on a Halifax-area mortgage would cause real financial strain, fixed is the safer choice. If you have cushion and can handle rate movement, variable remains a reasonable option.

For a broader look at how this rate environment is playing out in the Halifax market right now, see my Spring 2026 Halifax real estate overview.

How the 2026 Stress Test Actually Affects Your Budget

This is the piece most buyers underestimate and it has real consequences for what you can borrow.

Canada’s federal mortgage stress test still requires lenders to qualify you at the higher of your contract rate plus 2%, or the OSFI minimum qualifying rate of 5.25%. Because actual market rates have been well above 3.25% for years, virtually all buyers today are being tested at “your rate + 2%”, not the flat 5.25% floor.

What that looks like in practice:

- Offered a 3.69% fixed rate? Your lender must prove you can handle payments at 5.69%.

- Offered a 3.39% variable rate? You’re being tested at 5.39%.

That’s a significant qualification hurdle, but here’s the important flip side: a lower contract rate directly improves how much you can borrow.

Shaving 0.5% off your contract rate lowers your qualifying rate by 0.5%, which can add tens of thousands of dollars to your theoretical purchase budget. This is exactly why getting the best rate possible isn’t just about monthly savings, it also affects your approval ceiling.

OSFI has also factored in a 4.5x income guideline nationally, meaning high loan-to-income applications in Halifax-Dartmouth can hit a ceiling even if the GDS/TDS ratios technically pass at the stress-tested rate. If you want to understand how those ratios work and how to optimize yours before you apply, the complete GDS/TDS guide on this site walks through the math in plain language.

A Note on Rate Holds and the Pre-Approval Window

One underused tool in a rising-rate environment: the rate hold.

Most lenders will lock in today’s rate for 90 to 120 days while you shop. That means if you get pre-approved now at 3.7% fixed and rates move higher before you find a home, your locked rate is protected. If rates drop, you get the lower rate. It’s asymmetric protection in your favour and it costs nothing.

Getting pre-approved before you start seriously looking is one of the highest-leverage moves a buyer can make in the current market. It clarifies your real budget, gives you credibility with sellers, and protects you against rate movement during your search. Read more in the mortgage pre-approval guide for Halifax buyers.

Don’t Forget: What Happens Between Approval and Closing

Getting a great rate is step one. Protecting it through to closing day is step two.

Many buyers don’t realize that lenders re-check your financial profile before the final close — sometimes just days before you sign. A new car loan, a furniture financing plan, or even a new credit application can change your debt ratios enough to affect your rate or approval. For a full breakdown of what not to do after you’re approved, see Don’t Finance Anything Between Mortgage Approval and Closing Day.

The Bottom Line for Nova Scotia Buyers in Spring 2026

Mortgage rates in Nova Scotia are genuinely more favourable than they were at the 2023–2024 peaks. A rate with a “3” in front of it from a reputable broker or non-bank lender is achievable for strong files. Fixed gives you certainty; variable gives you a lower entry point and a bet on rate stability. The stress test still qualifies you at “rate + 2%” — so a better contract rate doesn’t just save you money monthly, it also expands your approval.

The key actions: shop the market rather than defaulting to your bank’s posted rate, get pre-approved early, lock in a rate hold, and keep your finances clean between approval and close.

And don’t forget, beyond your mortgage, there are closing costs when buying in Nova Scotia that need to be budgeted separately. Getting the full picture early prevents surprises on closing day.

Ready to talk through what your numbers look like in today’s rate environment? Contact Rob Lough for a no-obligation conversation. With 25 years of Nova Scotia real estate experience — including 5 years as a licensed Home Inspector — I help buyers navigate every part of the process, from pre-approval to keys in hand.

Related Resources

- Mortgage Calculator

- Why Getting Pre-Approved Is the Smartest First Step When Buying a Home in Halifax

- GDS vs. TDS Ratios: Your Complete Guide to Canadian Mortgage Qualification

- Don’t Finance Anything Between Mortgage Approval and Closing Day

- Spring 2026 in Halifax — Market Update

- Closing Costs When Buying in Nova Scotia