Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

What Killam’s Q1 2026 Results Tell Us About Halifax’s Rental Market

By Rob Lough, Broker/Owner | Century 21 Optimum Realty | Halifax-Dartmouth, Nova Scotia

When one of Canada’s largest apartment REITs reports its quarterly results, Halifax real estate watchers should pay attention. Killam Apartment REIT (TSX: KMP.UN) released its Q1 2026 financials on May 6, and the numbers offer a useful institutional lens on the same rental market conditions driving decisions by local landlords, investors, and would-be buyers every day.

Here’s what the data says and what it means if you own, rent, or invest in Halifax-area real estate.

Killam’s Q1 Numbers: The Headlines

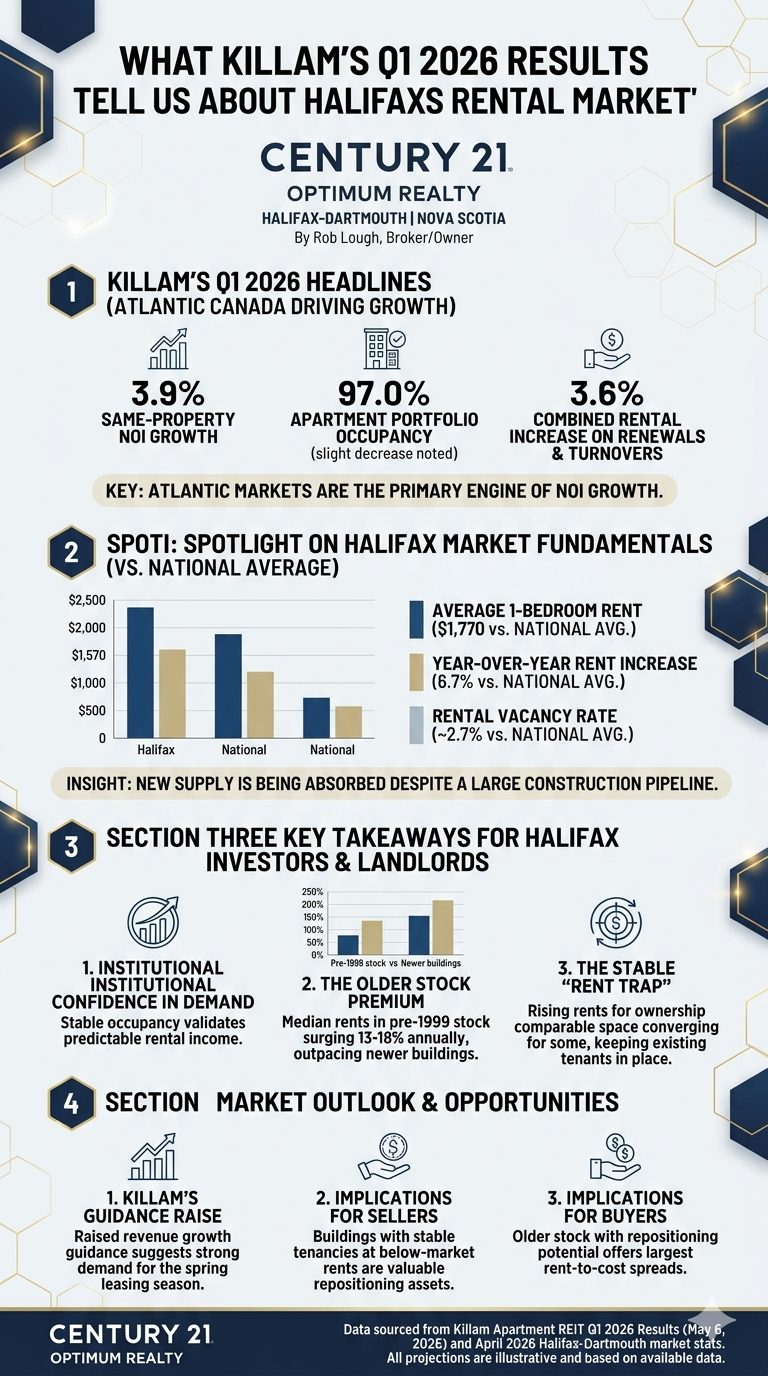

Killam delivered same-property net operating income (NOI) growth of 3.9% in Q1 2026, on the back of 3.6% same-property revenue growth. Occupancy across its apartment portfolio held at 97.0%, down just 40 basis points from Q1 2025. Rental rates on renewals and turnovers averaged a combined 3.6% increase for the quarter.

Adjusted funds from operations (AFFO) per unit grew 4.3% to $0.24, and the rolling 12-month AFFO payout ratio improved to 68% from 70% a year earlier — a signal of strengthening financial health. Total NOI reached $62.0 million, up 5.1% year-over-year.

In the words of CEO Philip Fraser: the Atlantic markets were the primary engine of that NOI growth.

That matters for Halifax.

Atlantic Canada Is Carrying the Portfolio

Killam’s geographic diversification spans Atlantic Canada, Ontario, Alberta, and BC, but management has been explicit that Atlantic Canada is doing the heavy lifting right now. Halifax’s fundamentals explain why.

Halifax one-bedroom apartments averaged $1,770 per month in early 2026, with year-over-year rent increases of approximately 6.7% outpacing the national average of 5.1%. Vacancy in the Halifax market remains tight at around 2.7% despite a significant construction pipeline. Those conditions give institutional landlords like Killam a durable revenue base — and they explain why Killam raised its 2026 same-property apartment revenue growth target to exceed 3.5% heading into the spring leasing season.

For a deeper look at how rent dynamics are evolving locally, my earlier analysis of how Halifax rent growth is shifting in 2026 covers the bifurcation between newer premium stock and older affordable units — a split that shows up clearly in Killam’s own commentary.

What 97% Occupancy Means for the Market

Killam’s 97.0% same-property occupancy is not just a corporate talking point. It reflects a structural reality: demand in Atlantic Canada is absorbing supply quickly enough that even well-managed, large-scale portfolios are running close to full.

That has two implications for local investors.

First, stabilized occupancy at this level means rental income is predictable. Vacancy allowances typically used in investment property analysis — often 5% to 10% of gross revenue — may be conservative in this environment, particularly for quality assets in Halifax proper, Dartmouth, and Bedford.

Second, it validates the supply picture. Despite Halifax housing starts jumping 32% year-over-year in 2025, most of that new supply has been multi-unit rental product rather than resale ownership housing. As I covered in the April 2026 Halifax-Dartmouth market stats, total active listings have climbed steadily, but rental vacancy has not followed at the same pace. New apartments are being absorbed.

For buyers: If you are evaluating an investment property in HRM, institutional occupancy benchmarks like Killam’s 97% are a useful reference point for underwriting assumptions. Older stock in established neighbourhoods is behaving differently from new premium towers — and that gap matters for your cash-flow model.

For sellers: Investment properties with solid tenancy records and below-market rents carry significant repositioning value right now. Understanding how to present that upside is part of effective pricing strategy.

The Older Stock Premium

One of the more compelling data points in the current market is what has happened to rents in pre-1999 rental stock. Median rents in Nova Scotia’s older rental inventory surged 13 to 18% annually between 2024 and 2025 — significantly outpacing the growth seen in newer purpose-built buildings, where asking rents have actually softened from 2024 peaks.

This inverts the usual logic. Newer buildings command higher absolute rents, but older buildings have seen faster percentage increases because their starting rents were so far below market. Landlords repositioning units in older buildings are capturing the largest rent-to-cost spreads available in the current cycle.

Killam itself flagged that demand for competitively priced units represents the strongest pressure point across their national portfolio. That is the affordable segment of Halifax’s rental market. It is also the segment where most mom-and-pop investor properties sit.

Does New Construction Actually Help Renters?

This is where Killam’s results connect to a broader housing policy question that comes up constantly in Halifax neighbourhood groups and planning meetings: if new buildings charge $2,350 or more for a two-bedroom, who are they actually helping?

New construction at the top end still commands a significant premium in Halifax — Killam’s own portfolio confirms it. But recent CMHC research on rental market filtering offers an important counterpoint to the “luxury only” argument. As I covered in Do New Apartments Actually Help Halifax Renters?, CMHC found that roughly one in three vacancies originating in a higher-rent Halifax building eventually cascades through a chain of moves to free up a lower-rent unit somewhere else in the region.

The mechanism is straightforward. When someone moves into a new building, they vacate an older unit. That vacancy gets filled by someone who vacates an even more modest unit, and so on down the chain. CMHC puts Halifax’s filtering probability at 33% — not a guarantee, but a real and measurable effect every time a new building opens.

What limits that effect in Halifax is in-migration. The city is growing at roughly 2% annually, which means a significant share of tenants moving into new buildings are arriving from outside the region entirely. Those moves don’t leave a Halifax vacancy behind, so the chain never starts. It’s an argument for continuing to build, but also for understanding that supply alone isn’t a complete affordability solution — which is exactly what Killam’s own commentary about persistently strong demand in the affordable segment confirms.

For landlords and investors, the practical takeaway is this: the softening at the top end of the Halifax rental market — which Killam is navigating with rental incentives now representing less than 0.9% of same-property revenue — does eventually apply downstream pressure on older stock rents. It hasn’t happened yet in any dramatic way. But it’s the directional force that filtering theory predicts, and Halifax’s construction pipeline is large enough to make it worth watching.

The Rent-to-Own Gap and What It Means for Sellers

One dynamic worth watching carefully is the narrowing gap between renting and owning. Halifax residential prices averaged around $610,000 in early 2026 with modest projected appreciation of 3% annually. At the same time, rents have risen enough that monthly carrying costs for ownership and monthly rent for comparable space are converging for some buyer profiles.

That convergence has two opposite effects. It makes ownership more compelling for renters who can access financing — the monthly difference between renting and owning is narrowing. But it also reinforces what some analysts call the “rent trap” dynamic: tenants already in place, especially those in older stock at below-market rents, have a strong incentive to stay put rather than giving up a fixed rent to enter a higher-cost ownership market.

For landlords, that tenant stability is a feature, not a problem. Low turnover rates reduce vacancy costs and leasing friction. Killam’s 5.0% turnover rental rate increase in Q1, while lower than 2025’s pace, still demonstrates that units hitting the market are repricing meaningfully upward.

For sellers of investment properties, understanding this dynamic is part of positioning an investment property competitively in Halifax’s spring 2026 market. A building full of long-term tenants at stable rents is an asset with a clear income story — one that sophisticated buyers will price appropriately if it is presented correctly.

Killam’s Guidance Raise: A Bellwether Signal

The most forward-looking element of the Q1 release was Killam’s decision to raise its 2026 same-property revenue growth guidance from 3.5% to greater than 3.5%. REITs do not revise guidance upward unless the leasing evidence coming in from the spring season supports it.

For Halifax, that signal matters. It means one of the most sophisticated, data-driven operators in the Atlantic Canada rental market is seeing stronger-than-expected demand entering the prime leasing season. That is consistent with what local brokers and property managers are observing on the ground.

Killam also noted that its capital allocation is currently focused on unit repurchases through its normal course issuer bid, buying back its own units below net asset value rather than deploying capital into acquisitions. That is a telling sign about where institutional money sees value right now — and it suggests that cap rates on quality Halifax apartment assets remain firm enough that Killam is not finding external acquisitions more attractive than buying its own portfolio at a discount.

What This Means If You Are Buying or Selling in Halifax

The Killam results do not change the immediate residential picture for Halifax homebuyers and sellers. The April 2026 Halifax-Dartmouth market data continues to show a normalizing market with rising inventory, more balanced buyer-seller dynamics, and prices that have held without collapsing.

But for anyone evaluating the investment side of Halifax real estate — whether as a landlord, a buyer of income property, or a seller trying to understand what drives value in multi-unit assets — Killam’s Q1 results are as good a market confirmation as you will find. Tight vacancy, rising rents, strong NOI growth, and raised guidance all point in the same direction: Atlantic Canada’s rental fundamentals remain among the strongest in the country.

For a full breakdown of current Halifax market conditions including home prices, rental vacancy, housing starts, and labour data, visit the Halifax Real Estate Market Dashboard.

Related Resources

- Do New Apartments Actually Help Halifax Renters? What CMHC’s Filtering Research Says

- Halifax Rent Growth Is Cooling in 2026 — But the Affordable End Remains Squeezed

- Halifax-Dartmouth Real Estate Market Stats: April 2026

- Spring 2026 in Halifax: What Buyers and Sellers Need to Know

- Purpose-Built Rentals Are Booming in Canada

- Canadian Housing Markets Aren’t Moving in Sync

Rob Lough is Broker/Owner at Century 21 Optimum Realty, serving Halifax Regional Municipality, East Hants, and the Truro/District 104 corridor. With 25 years of Nova Scotia real estate experience — including 5 years as a certified Home Inspector — Rob brings an unusually grounded perspective to both residential and investment real estate. Contact Rob to discuss buying, selling, or evaluating investment property in the Halifax-Dartmouth market.