Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

The Smith Maneuver and Cash Damming: A Canadian Real Estate Investor’s Guide 2026

By Rob Lough, Broker/Owner Century 21 Optimum Realty Halifax-Dartmouth, Nova Scotia

Most Canadian homeowners pay their mortgage with after-tax dollars and never think twice about it. But for Nova Scotia property owners who know where to look, the Income Tax Act contains a provision, Section 20(1)(c), that can turn a portion of your borrowing costs into a legitimate tax deduction. The Smith Maneuver and cash damming are two strategies built on exactly that foundation.

Neither is a loophole. Both are CRA-recognized, legally sound, and capable of producing meaningful long-term results for the right candidate. What follows is a plain-language breakdown of how each works, who qualifies, and how they can be combined for maximum effect.

What Is the Smith Maneuver?

The Smith Maneuver is a debt-conversion and wealth-accumulation strategy developed by financial planner Fraser Smith in the 1980s and popularized in his 2002 book. The goal is to convert your non-deductible residential mortgage into a tax-deductible investment loan, while simultaneously building an investment portfolio.

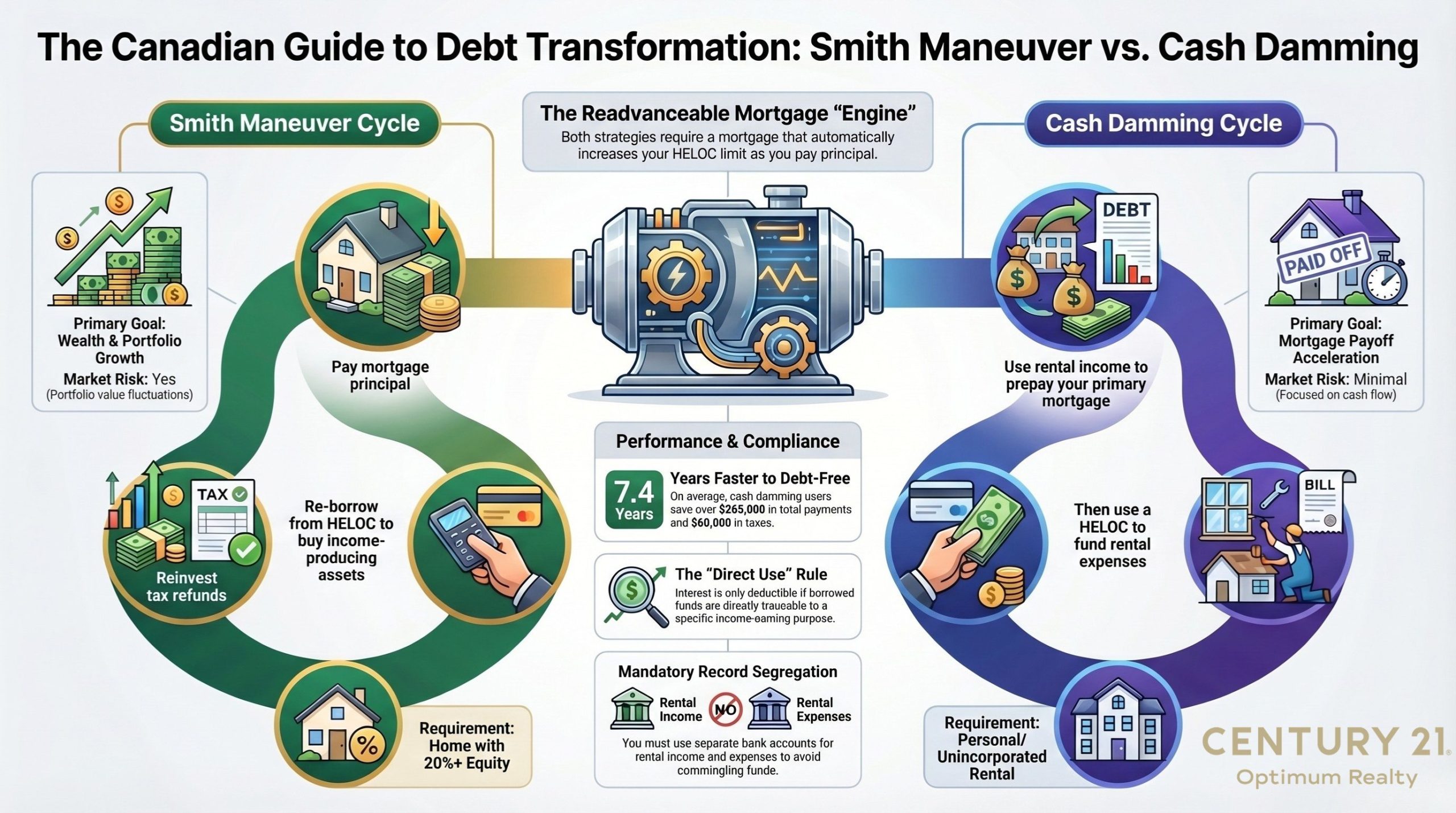

Under Canadian tax law, mortgage interest on a principal residence is not deductible. But interest on money borrowed to earn income from business or property is deductible. The Smith Maneuver exploits that asymmetry using a readvanceable mortgage: a mortgage bundled with a Home Equity Line of Credit (HELOC) that automatically restores your available credit as you pay down principal.

How It Works

Here is the core monthly cycle:

- You make your regular mortgage payment. The principal portion reduces your balance and simultaneously opens the same amount in HELOC room.

- You immediately re-borrow that amount from the HELOC and invest it in income-producing assets, dividend stocks, ETFs, bonds, or real estate.

- Because the HELOC funds were used to purchase income-generating investments, the HELOC interest is deductible under ITA 20(1)(c).

- The tax refund generated gets applied as a lump-sum prepayment against your original mortgage, freeing up even more HELOC room for further investment.

- Repeat monthly.

Over time, the original mortgage shrinks while the investment portfolio and tax-deductible HELOC balance grow. It is a self-reinforcing cycle.

The Math

At a 43.4% marginal tax rate, a $140,000 HELOC at 3% interest generates $4,200 in annual interest and roughly $1,822 back in tax savings. For someone in a 50% bracket borrowing at 7%, the effective after-deduction cost drops to 3.5%. The higher interest rates have been in recent years, the more valuable the deduction becomes.

Accelerators

The basic monthly cycle can be enhanced by applying existing investment assets against the mortgage then immediately re-borrowing and reinvesting, diverting monthly savings against the mortgage principal then re-borrowing the same amount, and using dividend income to prepay the mortgage before re-borrowing for additional investments.

What Is Cash Damming?

Cash damming applies the same core mechanics as the Smith Maneuver, but to rental property expenses rather than portfolio purchases. The CRA explicitly recognizes it in Income Tax Folio S3-F6-C1, which acknowledges fund segregation via cash damming as a valid method for tracing borrowed money to deductible purposes.

The strategy allows a rental property owner to use their rental income to attack their non-deductible personal mortgage, while using a line of credit to fund rental expenses, the interest on which is potentially deductible.

Who Qualifies

Cash damming requires either a primary residence with at least one separate rental property, or a primary residence where a portion is rented out such as a basement secondary suite. One important condition: the rental property must be personally owned, not held inside a corporation. The strategy must operate in your name only.

How It Works

You establish three separate accounts: a main chequing account linked to your primary residence mortgage, a dedicated rental income account where tenants deposit rent, and a dedicated rental expense account for each property funded only by line of credit draws.

The monthly cycle runs as follows. Tenant rent deposits into the rental income account. That rental income transfers to your main chequing account. A lump-sum prepayment of that amount goes against your primary residence mortgage. Because the mortgage is readvanceable, that principal reopens immediately as HELOC room. HELOC funds are drawn and deposited into the rental expense account. All rental property costs, mortgage payments on the rental, property taxes, condo fees, maintenance, utilities, insurance, are paid from that dedicated account.

The net result: your rental income is dismantling your personal mortgage faster, while borrowed money funds your rental expenses. The LOC interest is potentially deductible because those funds have a clear, traceable income-earning purpose.

What Rental Expenses Are Eligible

Eligible expenses that can be funded through the LOC, and for which the resulting interest may be deductible, include rental property mortgage payments and interest, property taxes, property management fees, maintenance and repair costs, condo fees, utilities paid by the landlord, and insurance premiums.

Real-World Results

According to data from firms actively managing cash damming for clients, average outcomes include mortgages paid off 7.4 years faster, approximately $265,000 in total payment savings, $68,000 in tax savings, and $57,000 in interest savings. Individual results typically fall in the range of 6 to 10 years off the mortgage term.

Smith Maneuver vs. Cash Damming: Side by Side

Requires rental property: Smith Maneuver, No, any homeowner qualifies. Cash Damming, Yes, rental income is the engine.

Source of deductible interest: Smith Maneuver, Borrowed funds invested in income assets. Cash Damming, Borrowed funds used to pay rental expenses.

Primary goal: Smith Maneuver, Wealth accumulation and investment portfolio. Cash Damming, Debt conversion and mortgage payoff acceleration.

Market/investment risk: Smith Maneuver — Yes, portfolio can decline. Cash Damming — Minimal, outcome tied to rental income.

Works for incorporated owners: Smith Maneuver — Yes. Cash Damming — No, personal ownership only.

Mortgage type required: Both require a readvanceable mortgage or HELOC.

Timeline predictability: Smith Maneuver, Less predictable, market-dependent. Cash Damming, More predictable, rental income-dependent.

Running Both Strategies Together

For a Nova Scotia rental property owner with a readvanceable mortgage, running both strategies simultaneously is the most powerful approach.

Cash damming runs on the rental side: rental income prepays your personal mortgage faster while the HELOC covers rental expenses and generates a stream of potentially deductible interest.

The Smith Maneuver runs on the investment side: as the primary mortgage is paid down faster by the cash damming prepayments, newly freed equity is re-borrowed and invested in income-producing assets, generating a second stream of potentially deductible interest.

The result is two distinct streams of potentially deductible interest, one tied to rental expenses, one tied to investments, while your personal mortgage is attacked from both directions. The combined structure does require that the two LOC components are completely segregated with separate tracking, as the CRA requires clean, independent tracing for each borrowing purpose.

CRA Rules, Risks, and Documentation

The Direct Use Rule

The CRA’s position, confirmed by the Supreme Court of Canada in Singleton v. Canada and Bronfman Trust v. The Queen, is that interest is only deductible when borrowed money is directly traceable to an income-earning use. Courts and the CRA do not accept overall balance sheet logic. The direct use must be demonstrable through records.

The GAAR Risk

Even technically compliant interest deductions can be denied under the General Anti-Avoidance Rule (GAAR) if the structure is found to be primarily for tax avoidance rather than genuine income-earning intent. Both strategies are considered CRA-compliant when implemented correctly, but they must be driven by legitimate investment or rental income goals, not solely by tax minimization.

Reasonable Expectation of Profit

For cash damming on rental properties, the CRA may challenge interest deductions if the property consistently reports losses. Rental properties must be operated with a genuine profit motive.

Documentation Requirements

Poor record-keeping is the single biggest risk factor in both strategies. Best practices include completely separate bank accounts for rental income, rental expenses, and the LOC with no commingling of personal funds. For every LOC advance, keep a corresponding invoice or receipt and proof of payment to a specific eligible expense. Save monthly statements for every account in the structure, and maintain a tracking spreadsheet capturing rental income received, mortgage prepayments, LOC withdrawals, LOC interest charged, and expenses paid. Plan mortgage renewals 4 to 5 months in advance and conduct an annual review of all transfer amounts.

Interest-Only LOC Payments

The LOC used in cash damming should be set up with interest-only pre-authorized payments. Repaying the principal would reduce the deductible portion of borrowing without improving tax efficiency.

What You Need to Get Started

A readvanceable mortgage. This is non-negotiable for both strategies. Products like Manulife One and Scotiabank’s STEP are common examples. The combined mortgage plus HELOC is typically capped at 80% of home value, and you generally need a minimum of 20% equity in your primary residence.

A rental property is required for cash damming, but not for the Smith Maneuver alone. For Nova Scotia investors exploring the Halifax rental market, it is worth understanding the MLI Select program for multi-unit financing and the regulatory landscape around starting an Airbnb in Halifax if you are considering short-term rental income.

Personal (unincorporated) ownership. Cash damming must operate in your personal name.

A qualified team. Both strategies require a real estate-focused accountant familiar with CRA interest deductibility rules and a mortgage broker experienced with readvanceable products. Understanding your full financing picture, including what rates look like in Nova Scotia today and how GDS/TDS ratios affect your qualifying position is essential before structuring any of this.

The Bottom Line for Nova Scotia Investors

Cash damming is purpose-built for rental property owners. It carries lower market risk, is more predictable in outcome, and can meaningfully accelerate your mortgage payoff by repurposing rental cash flows you are already receiving.

The Smith Maneuver is broader in scope and carries investment risk, but it can build a substantial portfolio alongside mortgage elimination, essentially converting your home equity into a working investment engine over time.

For a Nova Scotia rental property owner with a readvanceable mortgage and unincorporated property ownership, running both strategies in tandem, with rigorous account segregation and professional guidance, represents one of the most tax-efficient paths available.

If you are exploring income property ownership in Halifax-Dartmouth, East Hants, or the Truro corridor, connect with me directly to discuss what the current market looks like and how these strategies might fit your situation.

Related Resources

- MLI Select Program: CMHC Multi-Unit Financing Guide

- Starting an Airbnb in Halifax: The Regulatory Roadmap

- What’s a Good Mortgage Rate in Nova Scotia?

- Why Getting Pre-Approved Is the Smartest First Step

- Halifax-Dartmouth Real Estate Market Stats: March 2026

Disclaimer: This article is for general informational and educational purposes only and does not constitute financial, tax, or legal advice. The Smith Maneuver and cash damming are complex strategies with significant tax and legal implications that vary based on individual circumstances. Always consult a qualified accountant, tax professional, and mortgage specialist before implementing any strategy discussed in this article. Rob Lough is a licensed REALTOR® and Broker/Owner at Century 21 Optimum Realty. He is not an accountant, financial advisor, or tax professional. Nothing in this article should be relied upon as personalized advice.