Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Mini Home Financing in Nova Scotia: How to Finance a Resale Mini Home on Leased Land

By Rob Lough, Broker/Owner | Century 21 Optimum Realty | Halifax–Dartmouth, Nova Scotia

Mini homes in parks remain one of the last truly attainable ownership options in many Nova Scotia communities, especially in and around Halifax, Truro, and smaller regional centres. But when the mini home sits on leased land in a park, financing it is often much harder than buyers expect.

I’ve been working on mini home and park home transactions in Nova Scotia for years, and I see the same pattern over and over again: solid borrowers who could easily qualify for a standard house and lot discover that most lenders won’t touch a resale mini home on leased land. Knowing why that happens—and which lenders still have options—is the difference between closing on a park mini home and watching the deal collapse at the financing stage.

TL;DR: Can You Finance a Mini Home on Leased Land in Nova Scotia?

If you’re short on time, here’s the quick version:

-

Most big banks in Nova Scotia will not do a conventional mortgage on a resale mini home in a park on leased land.

-

Financing usually comes from credit unions, specialty manufactured‑home lenders, or by using equity from another property (for example, a HELOC or refinance).

-

You should expect higher rates, shorter terms, and bigger down payments, often 20–35% or more, than you would need for a typical insured mortgage.

-

Before you fall in love with a specific mini home, speak with a lender or broker who actively finances park minis in Nova Scotia and confirm your options.

For a broader primer on how different financing types affect closing costs, you can also read my guide to closing costs when buying in Nova Scotia.

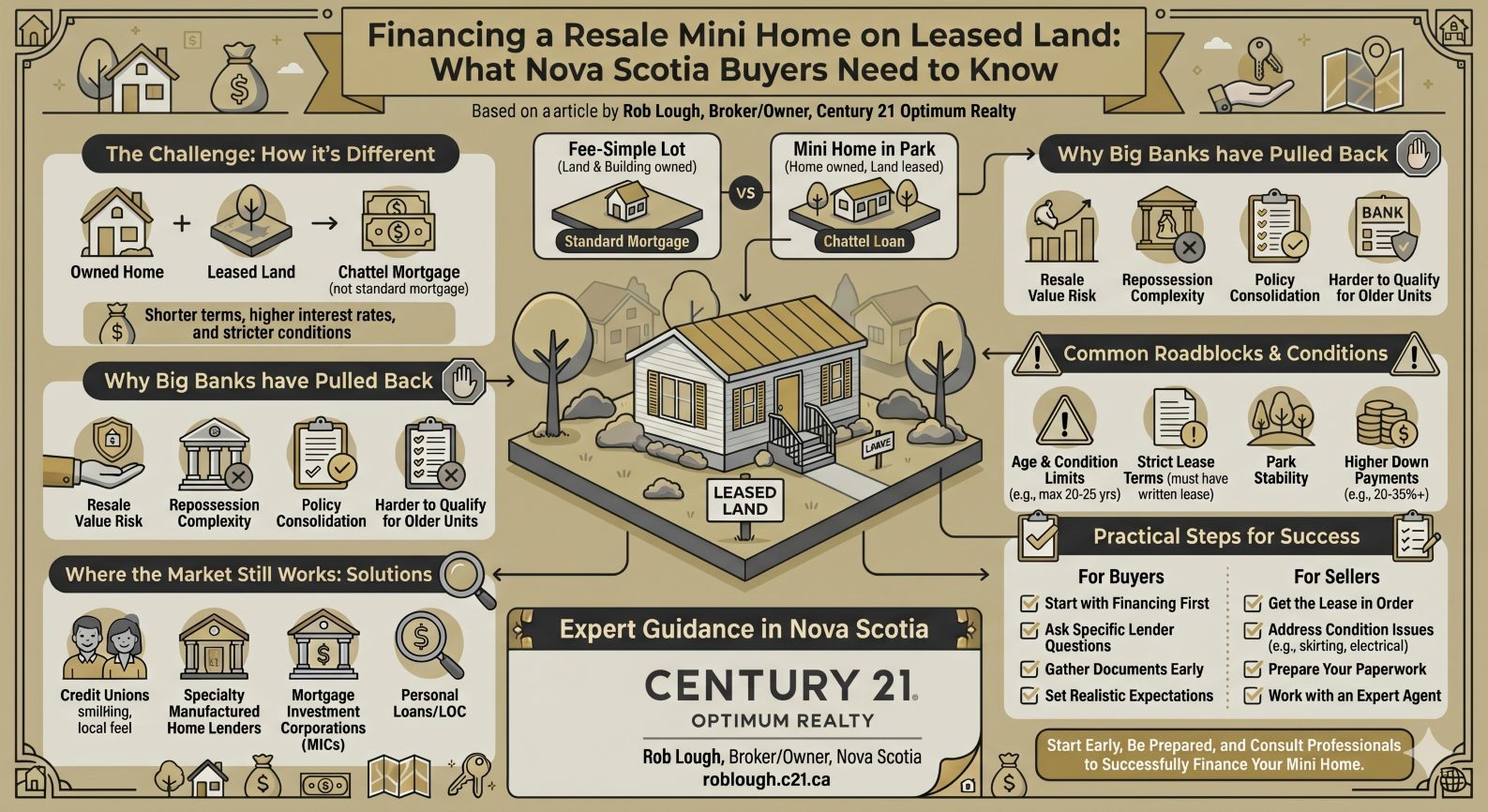

How Mini Home Financing on Leased Land Differs From a Regular Mortgage

The biggest difference is simple: you don’t own the land. When you buy a house on its own PID in Nova Scotia, the lender registers a mortgage against the land and building together, which gives them clear security if something goes wrong.

In a park, you own the mini home but lease the pad from the park owner, usually under a month‑to‑month or annual lease. There’s no land title available, so lenders can’t register a conventional real property mortgage. Instead, when they do lend, they typically use a chattel loan or collateral loan secured against the home itself, and they register that interest in the Personal Property Registry rather than the Land Registry.

Because the lender’s security is weaker and the resale market is thinner, terms are different too:

-

Rates are often higher than on a traditional mortgage for a house and lot.

-

Amortization periods are usually shorter (often 10–15 years instead of 25–30).

-

Loan‑to‑value limits tend to be lower, which means bigger down payments.

Why Big Banks Rarely Finance Resale Mini Homes in Parks

A few years ago, some major Canadian banks would occasionally finance resale mini homes in parks under specific conditions. That’s become much less common. Key reasons:

-

Resale value risk. Without land, it’s harder to project long‑term value, especially if pad rents increase or park rules change.

-

Repossession challenges. In a default, the lender may need to physically remove and relocate the home, coordinate with park management, and find a buyer in a narrow resale market.

-

Policy tightening. Most national lenders have standardized policies: manufactured homes on owned land may be fine, but older mini homes on leased pads often are not.

For buyers, that usually shows up as a very blunt answer at the branch level: “We don’t do mobile homes in parks.”

If you want a deeper dive on how banks look at value and collateral in general, my article on bank appraisals vs. real estate CMAs in Nova Scotia is a good companion read.

Mini Home Financing Options in Nova Scotia (Leased Land)

For a resale mini home in a park, most Nova Scotia buyers start with a credit union. Credit unions set their own policies and some still offer specific programs for manufactured and mobile homes on leased land. That said, policies vary widely: one credit union may be open to these deals, while another down the road will decline them all.

Beyond credit unions, you may encounter:

-

Mortgage Investment Corporations (MICs): Private lending funds that can be more flexible but usually lend at higher rates and over shorter terms.

-

Specialty manufactured‑home lenders: Niche lenders whose entire focus is mini, mobile, or modular homes, sometimes including park units.

-

Finance companies and consumer lenders: Can sometimes structure loans secured against the home, but at pricing closer to consumer credit than traditional mortgages.

None of these feel like a simple insured mortgage on a starter home—but they can still get a park mini home deal done when properly structured. If you’re also considering more conventional options in the same price range, my guide to Nova Scotia’s 2% down payment program explains how that pilot works for qualifying properties that do sit on owned land.

Common Conditions and Roadblocks for Park Mini Home Financing

Even when you find a lender willing to look at a park mini home, there are typical conditions that can derail approval:

-

Age limits. Many lenders cap the age of park mini homes they’ll finance, often around 20–25 years.

-

Pad lease terms. Lenders usually require a written, assignable pad lease, and they may want the lease term to run at least as long as the loan term.

-

Park stability. Questions around park ownership, rent‑increase history, replacement rules, and any closure risk can affect the lender’s comfort level.

-

Higher down payments. It’s common to see 20–35% down or more, particularly with MICs and specialty lenders.

This is one reason mini homes show up frequently in my Halifax–Dartmouth market stats discussions as an important but under‑served affordability segment.

How Mini Home Deals on Leased Land Typically Get Structured

When a park mini home financing package does come together in Nova Scotia, it usually looks like one of these structures:

-

Chattel loan through a credit union or specialty lender.

Secured against the mini home itself, registered in the Personal Property Registry, with terms often in the 10–15 year range and rates above standard mortgage pricing. -

Personal loan or unsecured/partially secured line of credit.

Used when the lender won’t treat the home as acceptable real estate collateral at all; approval is based on your personal covenant rather than the home. -

HELOC or refinance on another property.

Buyers who already own a house, condo, or multi‑unit property may refinance or draw on a HELOC, then purchase the mini home in the park with cash. If you’re weighing this strategy against buying a more traditional starter home, my piece on buying your first home in Truro, NS walks through how first‑time buyers often structure their financing.

Practical Steps for Buyers (and Their Agents)

The best advice I can give buyers looking at mini homes on leased land in Nova Scotia is simple: start with financing, not the home.

Before you book showings, do this:

-

Have very specific conversations with lenders or brokers. Ask directly: “Do you finance resale mini homes in parks on leased land in Nova Scotia?” and follow with questions about maximum home age, minimum purchase price, minimum down payment, and preferred term.

-

Gather documents early. Lenders will want the pad lease, park rules, proof of taxes and utilities, the serial number and CSA/build sticker, plus any major upgrade history.

-

Expect different terms than you’d see on a typical starter home. Shorter amortizations, slightly higher rates, and stricter age/condition rules are normal in this niche.

If you’re planning a purchase that might involve both a park mini home and a “regular” house as alternatives, or you’re weighing mini home ownership against staying in the rental market, it’s worth looking at my Halifax real estate and economic dashboard updates for a macro view of prices, rents, and incomes.

How Sellers Can Make Their Park Mini Home More “Financeable”

For sellers, the financing gap affects you too: if only a small fraction of buyers can finance your mini home, it impacts both your days on market and the offers you receive.

You can improve your odds by:

-

Cleaning up the lease. Make sure you have a clear, written, assignable pad lease with as much remaining term as possible.

-

Addressing obvious condition issues. Roof, skirting, electrical, and blocking/tie‑downs are key items for inspectors and lenders.

-

Organizing your paperwork. Have age, CSA certification, major upgrades, and any prior appraisals handy.

-

Working with an agent who understands mini home financing in Nova Scotia. Knowing which lenders are still active, and in what order to approach them, can directly affect whether your buyer’s financing holds together.

If you’re thinking about selling and want a broader framework for preparing your property, my page on selling your home with Century 21 Optimum Realty covers the step‑by‑step process and marketing strategy I use.

The Bigger Picture: Mini Homes, Affordability, and Nova Scotia’s Financing Gap

Park mini homes fill an important affordability gap in Nova Scotia’s housing system, especially outside the core Halifax market. They often represent the only ownership option below a certain price point for first‑time buyers and people on fixed incomes.

At the same time, Nova Scotia is dealing with a broader affordability and supply challenge, which I’ve written about in detail in my article on the massive first‑time buyer wave building in Canada. New construction, modular developments, and down payment assistance programs help—but they don’t fully address the lack of stable, predictable financing options for existing affordable stock like resale park mini homes.

A more robust chattel‑loan framework, with clear age and condition standards and consistent rules around leased‑land security, could safely bring more institutional lenders back into this space in Nova Scotia. That would broaden the buyer pool, stabilize values for existing park mini homes, and give more Nova Scotians a realistic path into ownership.

Frequently Asked Questions: Mini Home Financing in Nova Scotia

Can I get a mortgage for a mini home in a park in Nova Scotia?

Not usually through a major bank, and not a conventional mortgage registered on title. For a resale mini home on leased land, you’re typically looking at a chattel or collateral loan from a credit union or specialty lender, or using equity from another property via a refinance or HELOC.

Why won’t banks finance resale mini homes on leased land?

Banks prefer land‑backed collateral. When a mini home sits on a leased pad, they can’t register a standard mortgage on real property, and repossession is more complex if there’s a default. Over the last several years, most big banks have quietly exited this segment in Nova Scotia.

How much down payment do I need for a mini home in a park?

Plan for at least 20%, and in many cases 25–35% or more, depending on the lender, age of the home, and overall strength of your application. High‑ratio insured mortgage programs that allow 5–10% down generally do not apply to park mini homes.

What is a chattel loan and how is it different from a mortgage?

A chattel loan is secured against the home as personal property rather than against land and building together. The security is registered in the Personal Property Registry, terms are often 10–15 years, and interest rates usually run higher than on a conventional mortgage.

Are older mini homes harder to finance?

Yes. Most lenders have a maximum age threshold (often in the 20–25 year range), and homes beyond that can be declined even if the buyer is very strong financially.

Does the park lease matter to the lender?

Very much. Lenders typically require a written, assignable pad lease, and many want the remaining lease term to at least match the loan term. Month‑to‑month or verbal arrangements are frequent deal‑killers.

Is it harder to sell a mini home in a park because of financing?

In practice, yes. A limited lender pool means a smaller buyer pool, which can affect your price, time on market, and conditions. Sellers who have their lease, documentation, and home condition in order give buyers the best chance of securing financing.

The Bottom Line (and How I Can Help)

Financing a resale mini home on leased land in Nova Scotia is more complicated than financing a traditional house and lot—but with the right preparation and the right lender, it is still possible.

If you’re thinking about buying or selling a mini home in a park anywhere in Halifax Regional Municipality, East Hants, or the Truro corridor, and you’re not sure how the financing will work, I’m happy to walk you through your options. You can start by browsing my latest Halifax–Dartmouth real estate market stats or just reach out for a no‑obligation conversation.

Rob Lough is Broker/Owner at Century 21 Optimum Realty, serving Halifax Regional Municipality, East Hants, and the Truro/District 104 corridor. With 25 years of Nova Scotia real estate experience, including five years as a certified Home Inspector, Rob brings a grounded, practical perspective to every transaction. roblough.c21.ca

Related Resources