Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Spring 2026 in Halifax: What Buyers and Sellers Need to Know About Prices, Inventory, and Mortgages

By Rob Lough, Broker/Owner — Century 21 Optimum Realty Published: March 2026

Spring is historically Halifax’s busiest real estate season and 2026 is shaping up to be no exception. Whether you’re thinking about buying your first home, upsizing, downsizing, or selling while demand is strong, the next 60 to 90 days could be the most important window of the year.

Here’s what you need to know heading into spring and what to do about it.

Where Prices and Inventory Stand Heading Into Spring

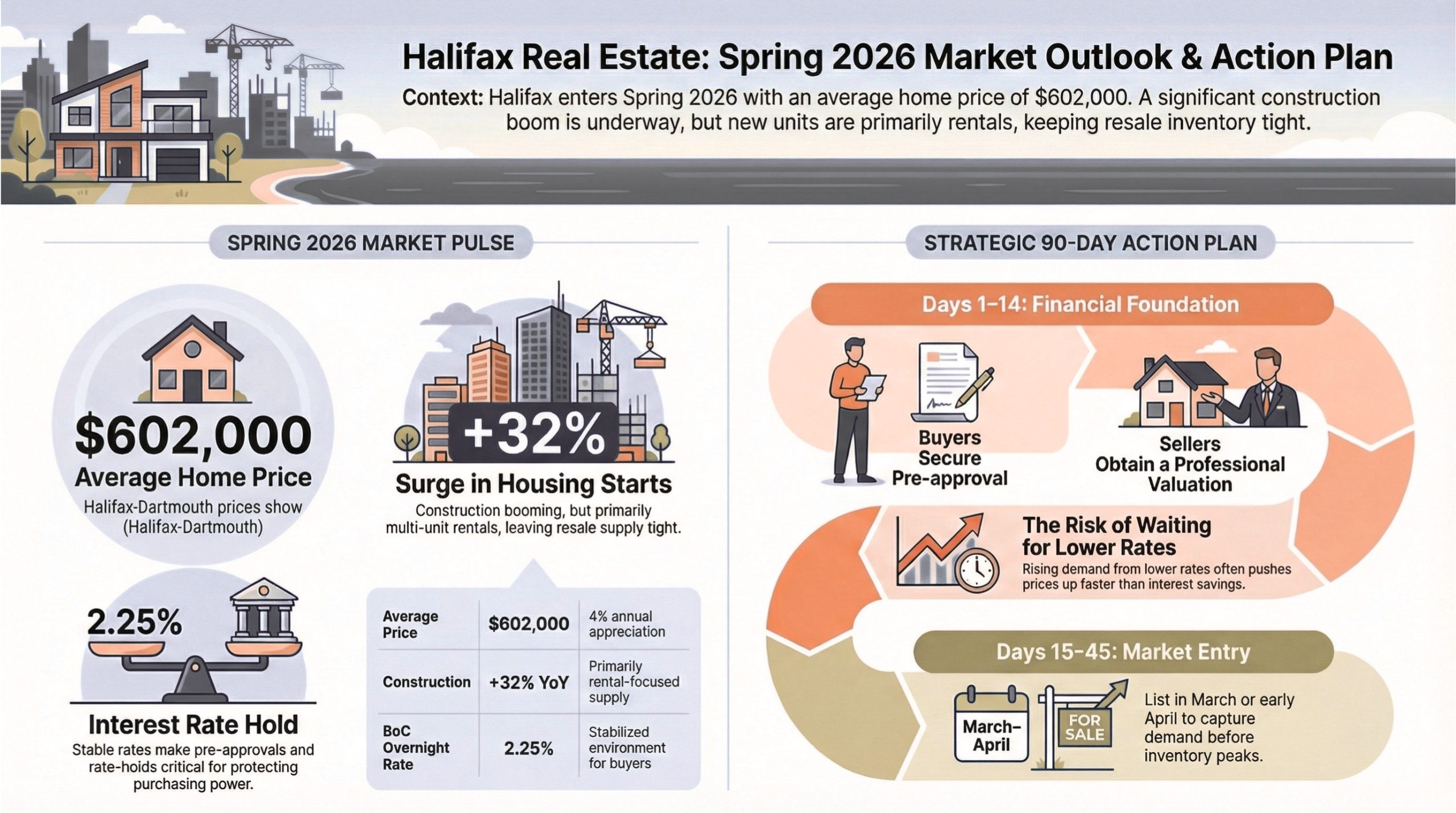

Halifax-Dartmouth entered 2026 on solid footing. As I covered in my Halifax-Dartmouth Real Estate Market Statistics 2025 year-end analysis, and my most recent analysis of the market stats for February 2026, the average home prices settled around $602,000 with healthy 4% year-over-year appreciation. The inventory picture, while showing some improvement, is still well below what most analysts would call a balanced market.

The Truro and Bible Hill market tells a similar story of strength heading into spring, with more homes selling, higher values, and properties moving faster than a year ago. Meanwhile, the District 104 analysis covering Truro, Bible Hill, and Stewiacke confirmed consistency and predictability across central Nova Scotia through the end of 2025.

On the supply side, Halifax housing starts jumped 32% year-over-year — one of the strongest construction booms in Canada. That new inventory will help over time, but most of it is multi-unit rental construction, not resale homes. Resale supply remains tight.

It’s also worth noting that Nova Scotia recorded its first quarterly population decline since 2020 in Q3 2025. While that could ease some demand pressure long-term, the current inventory gap is still wide enough to keep upward pressure on prices through spring.

For buyers: Inventory typically rises in April and May, giving you more choice — but more competition arrives at the same time. Early spring movers often face less competition than those who wait until the traditional peak weeks.

For sellers: Your leverage is strongest when inventory is still lean. Listing in March or early April, before the bulk of spring listings hit the market, can generate stronger multiple-offer situations and faster sales.

How Today’s Mortgage Rates Affect What You Can Afford This Spring

Mortgage rates are the single biggest factor in what a buyer can actually afford — and right now, the fixed-versus-variable decision is more nuanced than it’s been in years.

As I discussed in my article on the Bank of Canada holding the overnight rate at 2.25%, a rate hold might seem like non-news at first glance, but for buyers, sellers, and investors in Nova Scotia, it has real implications for purchasing power and market timing.

Five-year fixed rates have settled into a range that’s notably lower than the peaks we saw in 2023 and 2024, but they haven’t dropped as far or as fast as many buyers were hoping. Variable rates have come down more aggressively thanks to previous Bank of Canada rate cuts, but they carry the uncertainty of future adjustments.

Here’s what a mortgage broker would tell you right now:

- Fixed rates offer peace of mind and predictable payments. If you’re stretching your budget, locking in removes the guessing game. Understanding your GDS and TDS ratios is essential for knowing exactly how much you qualify for.

- Variable rates are currently lower, which means more purchasing power today, but you need to be comfortable with the possibility that payments could adjust.

- Pre-approvals and rate holds are critical this spring. A rate hold (typically 90 to 120 days) locks in today’s rate while you shop. If rates drop before you close, you get the lower rate. If they rise, you’re protected. I wrote about why getting pre-approved is the smartest first step that advice is even more relevant now.

Meanwhile, Canadian mortgage delinquency rates have ticked up slightly but remain remarkably low by historical standards — a sign that homeowners are managing their payments despite past rate hikes. That stability is good news for the overall health of the market heading into spring. Here in a note from Greg Matthews of TMG The Mortgage Group Atlantic:

I always recommend my clients connect with a trusted mortgage professional early not after they’ve found a home. You can start with our mortgage calculator to get a rough idea of your numbers, or get pre-approved right here.

Why Waiting for “Better Rates” Might Backfire

This is the conversation I have almost every week: “Should I wait for rates to drop more before I buy?”

It’s a reasonable question. But here’s the math most people overlook.

When rates drop, more buyers qualify. When more buyers qualify, demand rises. When demand rises — especially in a market that’s already short on inventory — prices go up. The monthly payment you were trying to lower by waiting for a better rate can actually increase because the purchase price climbed faster than the rate fell.

We saw exactly this dynamic play out across Halifax Regional Municipality in previous rate-cut cycles. The buyers who moved decisively when rates first started declining often got better overall deals than those who waited for the “bottom.”

As I outlined in my piece on how first-time buyers in Canada face a tougher climb than past generations, the affordability gap isn’t just about rates — it’s about how quickly prices can move in a supply-constrained market. Waiting often makes the gap wider, not smaller.

If the down payment is your biggest hurdle, it’s worth knowing about Nova Scotia’s 2% Down Payment Program, which can significantly reduce the upfront cash you need to get into the market.

For buyers: The best time to buy is when you can afford to and you find the right home. Trying to time both rates and prices perfectly is a strategy that rarely works out.

For sellers: Falling rates expand the buyer pool. Every quarter-point drop qualifies thousands of additional buyers across Nova Scotia. If you’re considering selling in 2026, spring positions you to capture that expanding demand before the market fully adjusts.

Your 60–90 Day Action Plan: Getting Ready to Buy or Sell This Spring

Whether you’re buying or selling, the most successful spring transactions start with a plan — not a panic. Here’s a practical timeline to get you positioned. For a deeper dive into budgeting and preparation, check out my guide on how smart planning makes homeownership possible in Nova Scotia.

If You’re Buying

Days 1–14: Financing First Connect with a mortgage broker and get fully pre-approved (not just pre-qualified). Lock in a rate hold. Understand your maximum budget and your comfortable budget — they’re not always the same number. Make sure you also understand the closing costs when buying in Nova Scotia so there are no surprises at the finish line.

Days 15–30: Define Your Search Work with your Realtor® to define your must-haves, nice-to-haves, and dealbreakers. Set up automated listing alerts so you’re seeing new properties the moment they hit the market. Review recent comparable sales so you understand pricing in your target neighbourhoods.

Days 30–60: Active Search and Offers Tour properties, attend open houses, and be ready to move quickly on the right one. In a competitive spring market, hesitation costs opportunities. Your Realtor® handles market strategy — pricing analysis, offer structure, negotiation. Your broker handles financing — conditions, timelines, and closing logistics.

Days 60–90: Closing and Possession Home inspection, appraisal, financing conditions, legal review, and the move itself. A coordinated team makes this process smooth rather than stressful.

If You’re Selling

Days 1–14: Strategy and Preparation Meet with your Realtor® for a free home valuation to understand what your property is worth in today’s market. Discuss pricing strategy, timing, and what — if any — preparation or staging will maximize your return. If you’re curious about the difference between a formal appraisal and what I provide, I’ve explained bank appraisals vs. real estate CMAs in detail.

Days 15–30: Get Market-Ready Complete any agreed-upon updates, declutter, deep clean, and arrange professional photography. First impressions drive showings, and showings drive offers. Keep in mind that rising property assessments across Nova Scotia are a reflection of real market value growth — your home may be worth more than you think.

Days 30–45: Launch to Market Hit the MLS at the optimal time for your neighbourhood and price range. Your Realtor® manages the marketing plan, showing schedule, and buyer inquiries.

Days 45–90: Offers, Negotiation, and Closing Review offers, negotiate the best terms (not just the highest price — closing dates, conditions, and deposits all matter), and move through to a successful closing.

Let’s Build Your Spring Plan Together

I’ve been helping buyers and sellers across Halifax Regional Municipality, East Hants, and Truro navigate every kind of market for over two decades. Whether this is your first purchase or your fifth sale, the fundamentals are the same: preparation, strategy, and the right team.

I handle the market side,pricing, negotiation, and timing. Your mortgage broker handles the money side, rates, approvals, and affordability. Together, we make spring 2026 work for you. The April 2026 Halifax-Dartmouth market stats are now live, see how the spring numbers compare.

Ready to get started? Contact me today for a no-obligation conversation about your spring real estate goals.

Related Resources

- Halifax-Dartmouth Real Estate Market Statistics 2025

- Halifax-Dartmouth Real Estate Market Statistics February 2026

- Truro-Bible Hill Real Estate Market Stats — January 2026

- Bank of Canada Holds Overnight Rate at 2.25%

- First-Time Buyers in Canada Face a Tougher Climb Than Past Generations

- Nova Scotia’s 2% Down Payment Program

- Why Getting Pre-Approved Is the Smartest First Step

- Free Home Valuation — What’s Your Home Worth?

- Mortgage Calculator

- Closing Costs When Buying in Nova Scotia

Rob Lough is a Broker/Owner and REALTOR® at Century 21 Optimum Realty, serving the Halifax Regional Municipality, East Hants, and Truro markets. With 25 years of Nova Scotia real estate experience — including 5 years as a licensed Home Inspector — Rob brings a uniquely grounded perspective to buying, selling, and market analysis.